The U.S. share of global venture investment has held steady at around 50% for the past five years. It was 51% in 2020. While this is down from an 84% share in 2004, and 90%+ share throughout the 1990s, high-growth tech companies with global market opportunities and unicorn potential would nonetheless be foolish not to consider the possibility of accessing the U.S. VC market.

There’s just one catch. Early stage (Seed and Series A) investors in the U.S. are seldom interested in investing in a foreign entity. For a myriad of tax (e.g., the capital gains tax benefits of owning Qualified Small Business Stock), governance, and legal reasons, they will only invest in U.S. corporations. Not only that, but they almost universally insist on investing in U.S. corporations incorporated in Delaware. Fortunately, there is a relatively simple way to accommodate this requirement – a transaction that is colloquially referred to as a “Delaware Flip”.

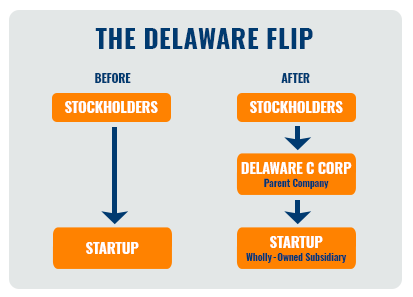

The Delaware Flip

A “Delaware Flip” transaction creates a U.S. holding company to acquire via a like-for-like stock swap of all the capital of the international operating company, thus resulting in the international company becoming a wholly owned subsidiary of the U.S. entity.

The following chart shows the impact on the corporate entity structure:

The U.S. venture fund is then free to invest in the newly created American company.

Other Conditions Precedent to Getting Funded

It is important to note that while the establishment of a U.S. holding company is often a necessary condition for U.S. investors to lead a Seed or Series A financing, it is likely not the only requirement. Investors may also require the establishment of a significant U.S. dimension to the operations of the company. This could include:

- Demonstrated traction in the U.S. market

- The presence of senior management (e.g., the CEO) in the U.S.

- The ownership rights in IP being transferred to the U.S. entity

- Etc.

Advantages of a Delaware Flip

There are several potential advantages that should be considered:

- The U.S. VC markets are still the deepest, most liquid, and most agile in the world.

- The premiere VC firms in the U.S. provide more than just access to capital, but also:

- strategic management support,

- access to market partners and,

- potentially better exit opportunities.

The U.S. therefore remains the optimum country in which to raise growth capital.

Disadvantages

There are several potential disadvantages that should be considered:

- Aggregate corporate tax rates in the U.S. are among the highest in the world and are expected to increase further. For early-stage companies, this may not be much of a concern, but the long-term implications should be considered.

- A Delaware flip is likely not reversible.

- Depending on the country of origin, implications for capital gains taxes should be considered.

- Many countries have their own tax incentives for early-stage companies (e.g. the UK’s Seed Enterprise Investment Scheme (SEIS) and Enterprise Investment Scheme (EIS)), and care should be taken to ensure the benefit of these programs is not negatively impacted by a change to foreign ownership.

- The ever-expanding scope of the administrative state should also be considered. Non-U.S. investors making equity investments into many U.S. companies are required before closing to file their investments with the Committee on Foreign Investment in the United States (CFIUS). It is unlikely that CFIUS’ requirements will become less intrusive over time.

- This is not a DIY transaction. It is essential to engage with suitably qualified attorneys and tax advisors in both countries to ensure a smooth transaction and avoid potentially disastrous consequences. The cost of executing the Delaware Flip transaction will likely run in the tens of thousands of dollars.

To Flip or Not to Flip? That is the Question

One of the most important deciding factors in determining how to set up North American operations is whether U.S. venture capital funding is anticipated to be a necessary part of the equation. If the answer is “yes,” then a Delaware Flip should be contemplated.

On the other hand, conventional wisdom is that a larger percentage of later stage investors (Series B+) are willing to invest in foreign entities. So, timing of anticipated funding rounds versus the go-to-market plan should be considered.

If the foreign entity does not need equity investment from U.S. investors, it does not necessarily have to do a “Delaware Flip.” It might be better to create a Delaware subsidiary of the foreign parent.

To make an informed judgment requires careful financial planning to establish the timing of funding requirements and the best sources of capital, along with thoughtful discussions with potential U.S. investors, attorneys, and tax advisors to understand the implications for the company, its employees, and its existing investors.

How vcfo Can Help

If you are a foreign company looking to expand into the U.S. market and/or to raise institutional growth equity in the U.S., vcfo can help with the following: the accounting and financial planning to support that transaction, introductions to trusted legal and tax advisors, C-suite recruitment, and taking care of your ongoing financial and HR requirements on a fractional basis.