Options to fund a business range from family and friends to banks to institutional capital and business owners are best served by understanding the advantages and disadvantages of each option before making this decision. Read more below for tips on navigating this process effectively.

Overview of the Stages:

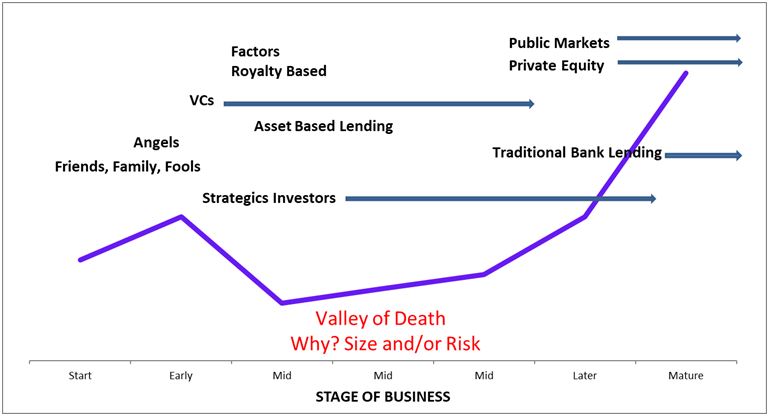

Even though every company has a timeline, the length at which they spend at each stage will be unique. Below is a chart indicating typical funding options for various stages of business. The purple line represents the relative chance of funding success.

- Start or ‘Idea’ stage, is where the business first starts to get off of the ground.

- Early stage typically has a commercialized product or service offering, early revenue, usually not yet turning a profit.

- Mid stages are where the company hits a growth curve, has meaningful revenue, reaches profitability and/or develops significant hard assets like receivables, inventory and fixed assets.

- Later is sustained profitability and growth.

- Much Later is a mature business

Financing Sources

Friends, Family, Fools: Young companies often rely on trusted relationships between the founders and their community. As many new businesses are not mature enough for other sources of financing, investments from relatives or friends help entrepreneurs get their ideas off the ground.

Angel Investors: Angel Investors often fund small, young, businesses or startups. Angels are individuals, usually business professionals, looking for higher rates of return. You tend to give up less control with Angels than you would with a Venture Capital (VC) firm. As with friends and family, you are usually working with smaller individual investments, and it can be hard to cobble together a meaningful amount of money. While you may benefit from the involvement and advice of an accomplished professional Angel Investor, it can also feel like herding cats. Angel capital is often an intermediate step to institutional venture capital.

Venture Capital: VCs look for high growth potential in small to medium sized businesses, typically a scalable technology-related business in a market they see as exceeding $500 million in annual revenue. Most businesses are not candidates for venture capital, and even if you are, there is no guarantee you will get funded by a VC. Also, an owner gives up a lot of control to the venture capitalist. However, if you are a candidate for VC funding, it can be a powerful source of meaningful amounts of capital and really help push a business forward.

Factors: A factor effectively buys a company’s receivables at a discount as sales are made. A company must have clean receivables and strong gross margins for factoring to work. This is expensive money, a form of debt for companies that are desperate but not too desperate. Companies who succeed will graduate to Asset-Based Lending (ABL) and/or traditional bank financing. It is common to see factoring in a small company selling a high margin product or service into larger companies who pay but pay slowly.

Royalty Based: Another expensive form of financing, the financing source makes an advance, similar to the initial funding of a term loan. The source is repaid out of a percentage of revenue, effectively a royalty over some period of time. The company must also have strong gross margins for royalty based financing to work.

Asset Based Lending (ABL): A step between factoring and traditional bank lending and priced in between. ABL lenders advance against receivables, typically weekly and the company directs its customer payments into a lock box controlled by the lender. The idea is that at any point in time, the lender can be made whole simply by collecting money that rolls into the lock box. This requires strong systems and good receivables and can be administratively burdensome. Equipment financing also falls under ABL, typically term loans or leases. Some banks have ABL departments.

Traditional Bank Lending: Traditional bank financing is the lowest risk to the lender and is is the least expensive for the borrower – if you qualify. For a business with two or more of the following: profitability, positive cash flow, assets or a strong guarantor. This type of financing can be in the form of term loan(s) secured by real estate or equipment or it can be a line of credit secured by accounts receivable and/or inventory. Banks usually require owner guarantees of a closely held business and the business to maintain financial covenants. Two government guarantee programs with bank lending: Small Business Administration (SBA) – where the government partially guarantees small business term loans and Export-Import Bank (EXIM) – where the government guarantees foreign accounts receivable for US exports. These programs can sometimes support a credit the bank would otherwise have a hard time doing alone.

Private Equity: Once a company has matured and proven itself as profitable, sustainable and on a growth path, Private Equity (PE) becomes a possible source. This can be in the form of equity or subordinated debt with equity kickers. The classic PE play to is buy or invest in a company, leverage with as much bank debt as possible, grow organically and through bolt-on acquisitions and sell at a higher revenue level and a higher multiple. As a close cousin to VCs, the business seeking to fund gives up a lot of control.

Strategic Investors: A strategic investor is a larger company with an interest in your product or service beyond purely “financial” and may want to acquire you some day or conduct a deal where they incorporate your product or service into theirs. Sometimes Strategic Investors are less sensitive to valuation than a VC but can be more bureaucratic to work with over time. They also often invest alongside venture capitalists.

Public Markets: The final stage (but an entry into the wider world of sourcing) is the public market. Usually, for later stage companies, this is a less expensive option than VC or PE money with a significant cost in reporting and compliance. Many entrepreneurs dream of taking their company through an “IPO” or Initial Public Offering. An IPO is a large expensive undertaking, and SEC reporting and compliance after the IPO can be challenging.

Vendor and Customer Financing: Not on the chart, Vendor and Customer financing are often overlooked and can come into play all along the spectrum. I once had a client that was cash-starved, but its contract manufacturer was cash-rich, and badly needed sales volume. A deal was worked whereby the vendor, the contract manufacturer, gave very favorable payment terms in exchange for a higher price – a win-win for both companies.

Surviving “Death Valley”

The valley or death exists for a company because, it has reached a place where it needs more capital than it can get from friends, family, and angels; it is not a candidate for or has been unable to get VC financing, it is not mature enough for private equity, or it is not low risk enough for the banks. Factoring, ABL, and Revenue-Based Financing are all niche products that may or may not fit.

In my experience, there is no magic bullet. At vcfo, we bring an intimate understanding of the different types of financing and the attributes required of each. As a business owner, you have to take honest stock of your strengths and weaknesses as they apply to various financing sources. You spend your efforts on sources that are fit for you and sometimes adjust your business strategy to what is feasibly available. We can help you evaluate your financing options as well as package, position and present your story.

Can we help you develop your own timeline? Contact me to discuss further.